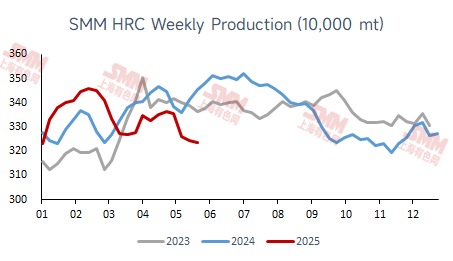

- HRC production showed a downward trend in May, with the rolling sample size nearly 4% lower than last year.

According to SMM data, the average weekly HRC production in May was 3.274 million mt. This week, HRC production was 3.2338 million mt, down 11,400 mt WoW. Compared to the same period in previous years, current HRC production was 7.08% lower YoY. Based on the latest rolling sample of weekly HRC production released by SMM, current HRC production was 3.9835 million mt, down 3.72% YoY.

- Decline in production schedule, increased impact from maintenance, and weak profitability advantage led to a decrease in HRC production in May.

Since the beginning of May, HRC production has continued to decline, primarily due to the combined effects of reduced production schedules at steel mills, concentrated maintenance activities, and a decline in profitability advantage.

From the perspective of production schedule, according to the latest tracking by SMM, the planned production volume of hot-rolled commodity materials for 39 mainstream steel mills producing HRC in May totaled 14.1287 million mt, with a daily average of approximately 455,800 mt. This represents a decrease of 13,300 mt from the actual daily average production of hot-rolled commodity materials in April, a decline of 2.8%.

From the perspective of maintenance, the impact from HRC maintenance in May is temporarily estimated at 968,800 mt, an increase of 223,500 mt MoM from the previous month. The increase in the impact from maintenance at steel mills in east China, north China, south China, and western regions is one of the main reasons for the decline in production.

In addition, from the perspective of profitability, the average SMM HRC profit in May was 130.84 yuan/mt, while the average rebar profit was 107.43 yuan/mt. The relatively close profit margins between HRC and rebar have resulted in low enthusiasm among steel mills to increase HRC production, with some steel mills actively adjusting the flow of pig iron. Under the combined impact of these factors, HRC production has continued to decline in May.

- HRC production in June is expected to increase MoM.

In terms of maintenance, according to the SMM survey, the domestic impact from HRC maintenance in June is temporarily 427,000 mt, a decrease of 541,800 mt MoM from the previous month. The impact from maintenance has significantly declined, and the resumption of production by steel mills after maintenance may drive a rebound in HRC production in June. However, considering the entry into the traditional consumption off-season, the market is cautious about demand expectations for June. Additionally, with the recent continuous weakening of steel prices and a decline in steel mill profits, the average HRC production in June is expected to be around 3.3-3.33 million mt.

![Before the holiday, the black chain is unlikely to see a trend-driven market [SMM Steel Industry Chain Weekly Report].](https://imgqn.smm.cn/usercenter/zUFfM20251217171748.jpg)

![[SMM Chromium Daily Review] Inquiries and Transactions Weakened, Chromium Market Showed Mediocre Performance Before the Holiday](https://imgqn.smm.cn/usercenter/ENDOs20251217171718.jpg)